Buying a Home in Ontario? The FHSA Rules You Can’t Miss test edit

Updated: June 2026

Estimated Read Time: 7 min

Ontario, Canada

What is FHSA, and Why Should First-Time Home Buyers in Canada Care?

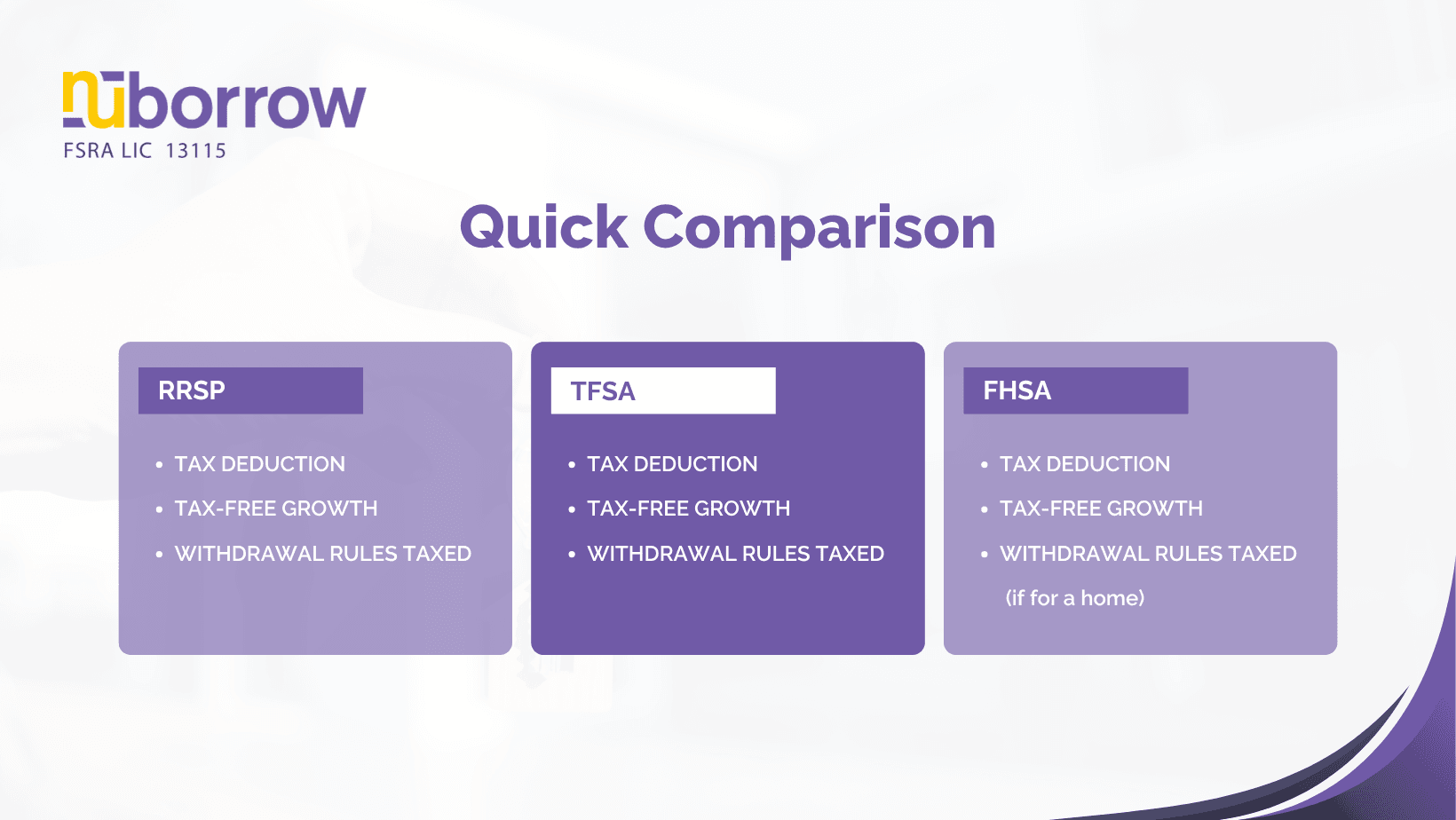

Registered Retirement Savings Plan (RRSP) First Home Savings Account (FHSA) Tax-Free Savings Account (TFSA)

For anyone dreaming of buying their first home in Ontario, the First Home Savings Account (FHSA) is a total game-changer. Launched by the federal government to help first-time buyers, it combines the best of an RRSP and a TFSA. That means you can save for your first home, tax-free. Here's the big news: The new FHSA contribution limits in Canada have been adjusted to keep up with inflation and housing costs. The yearly contribution limit remains $8,000, but there are strategic ways to use it that weren’t as clear before.

FHSA Contribution Limits in Canada: The Basics

Let’s keep it simple so you don’t get misunderstood. This is where most first-time buyers mess up. You can contribute up to $8,000 per year, with a lifetime max of $40,000, and the best part is that contributions are tax-deductible. That’s right, you can reduce your taxable income and save for a house.

Key FHSA Rules:

-

Annual limit: $8,000 (no increase as of June 2025)

-

Total lifetime cap: $40,000

-

Tax-free growth on all investment earnings within the FHSA

-

15-year use period, or until age 71, whichever comes first

-

Carry-forward: Up to $8,000 unused room (max)

-

Max contribution in a single year (with carry-forward): $16,000

What most people misunderstand

-

Contribution room starts only after you open your FHSA — not automatically at age 18

-

You can’t stack unlimited unused room like a TFSA — only one year ($8K) carries forward

-

Over-contributing triggers a 1% monthly penalty tax

How to Use FHSA to Buy a House in Ontario

So, how does it help you get your first home? Here’s the smart play:

-

Open your FHSA (most banks and online platforms offer it).

-

Contribute up to $8,000 per year or roll over from your RRSP.

-

Use it when you're ready to make a down payment. No taxes, no penalties.

Example: Let’s say you contributed $8,000 a year for 5 years. That’s $40,000 in savings + tax benefits. If you’ve invested wisely inside the FHSA, your savings could grow to over $50,000+, all available for your first home in Ontario.

FHSA vs RRSP: What’s Better for First-Time Buyers?

While both the FHSA and RRSP help you save for a home, they’re built differently: Feature FHSA RRSP (Home Buyers’ Plan) Contribution Limit $8,000/year (up to $40K total) $35,000 (one-time withdrawal) Tax Deduction ✅ Yes ✅ Yes Tax-Free Withdrawals ✅ Yes (for qualifying home) ❌ Must repay over 15 years Repayment ❌ Not required ✅ Required

Advice: Use FHSA first. Then go into the RRSP if you've maxed it out. The RRSP Home Buyers' Plan is a solid backup, but it needs planning and repayments.

Why It Matters for Ontario Buyers in 2026

Ontario’s housing market continues to challenge first-time buyers. Prices are high, interest rates are uncertain, and every dollar counts. The FHSA is one of the few tools that gives you a head start without the tax burden. This is especially helpful for Toronto, Mississauga, Ottawa, and other surrounding cities where average home prices are over $600,000.

FAQs

What counts as a “first-time home buyer” in Canada?

You’re considered a first-time buyer if you haven’t owned a home in the last 4 years.

What is the FHSA in Canada?

The First Home Savings Account (FHSA) is a registered savings account that helps first-time home buyers save for a home with tax-deductible contributions and tax-free withdrawals.

What is the FHSA contribution limit in 2026?

The annual limit is $8,000, with a lifetime maximum of $40,000.

Do I need to repay FHSA withdrawals?

No. Unlike RRSP withdrawals under the Home Buyers’ Plan, FHSA withdrawals do not need to be repaid.

Can I open both an FHSA and use the RRSP Home Buyers’ Plan?

Yes! You can combine both programs, just make sure you understand how each affects your taxes and repayment.

What happens if I don’t buy a home within 15 years?

You can transfer your FHSA funds to an RRSP or RRIF tax-free — no penalties.

Lastly

If you're buying a home in Ontario in 2026 and you're not using an FHSA, you're basically leaving free money on the table.

- The smartest move right now:

- Open your FHSA early

- Max out contributions annually if possible

- Pair it with RRSP strategically

- Because in this market, it’s not just about saving, it’s about saving smart and tax-efficiently.

FHSA isn't just a savings account; it's a powerful strategy for smarter homeownership. Every dollar you save tax-free helps you fight rising home prices and rate hikes.

Nuborrow offers expert mortgage solutions tailored to first-time buyers in Ontario. Talk to our Mortgage Expert

About the Author

Content team at Nuborrow, specializing in Canadian housing, lending trends, and first-time buyer education. They create clear, practical content that helps Canadians, especially in Ontario, make confident, well-informed home financing decisions. They know better about FHSAs, mortgage approvals, and interest rate changes into easy-to-understand guidance that aligns with real market conditions.

Disclaimer

This content is for informational purposes only and reflects general guidelines based on current Canadian housing and tax rules as of 2026. It does not constitute financial, legal, or tax advice. FHSA rules, contribution limits, and eligibility criteria are set by the Canada Revenue Agency and may change over time.

Related Articles

Buying a Home in Ontario? The FHSA Rules You Can’t Miss test edit

April 02, 2026 (4 mins read)

New FHSA rules in Ontario for 2026 help first-time buyers save smarter. Learn about contribution limits, tax-free savings, and how to use an FHSA to buy a home.